We are now more than halfway through the year and the stock market continues the ascent that began in 2009. One of the most significant events in the quarter was the Federal Reserve’s decision to increase short-term interest rates again. This was an appropriate action given the economy is doing well enough to warrant rates above zero, where the Fed held them between 2008 and 2015. Of the Fed’s two mandates, full employment and stable prices, both are currently hitting their targets.

We are now more than halfway through the year and the stock market continues the ascent that began in 2009. One of the most significant events in the quarter was the Federal Reserve’s decision to increase short-term interest rates again. This was an appropriate action given the economy is doing well enough to warrant rates above zero, where the Fed held them between 2008 and 2015. Of the Fed’s two mandates, full employment and stable prices, both are currently hitting their targets.

Around this point in the business cycle, when the unemployment rate is low, one fear that comes up is accelerating inflation. This quarterly commentary focuses on the phenomena of inflation, which famed economist Milton Friedman once described as taxation without legislation.

What is inflation?

On a basic level, inflation is the general rise in prices of goods and services. Inflation is usually mentioned in a negative light, eliciting images of hyperinflation and needing a wheelbarrow full of cash to buy a loaf of bread. A little inflation, however, is considered healthy for an economy, as long as wages are growing too. When inflation gets too high though, it’s a sign the economy is overheating and is usually a precursor to the next downturn. A decline in prices, or deflation, on the surface, sounds good. Who wouldn’t want to pay less for goods and services? The reality is though, that in a deflationary environment, people pull back on spending because they can purchase things at a lower price in the future, which causes the economy to weaken. If people think prices will be higher in the future, it can pull forward spending and spur economic growth. This is why inflation is like Goldilocks, we don’t want it too hot or too cold, but somewhere in the middle. In fact, the Federal Reserve’s stated target is an inflation rate of 2%.

Why is inflation important to you?

Sustained inflation over time reduces the purchasing power of money. For example, $1 fifty years ago would be worth $0.13 today. Said another way, something that cost $1 in the ‘60s would cost $7.52 today (this is that taxation without legislation concept). One of the main purposes of investing is to have assets keep up with, or preferably, outpace inflation. This is why in financial planning we talk about the assumed “real” rate of return, or the return over inflation one needs to meet one’s goals. As an example, if we are using an assumed rate of return in a financial plan of 5% and applying a 3% inflation rate to spending, what we are saying is the target portfolio return is 2% over whatever inflation ends up being. This is why we spend a lot of time researching the level and direction of inflation. That information can drive portfolio changes since certain types of investments do better than others in various inflationary environments.

What is our research telling us?

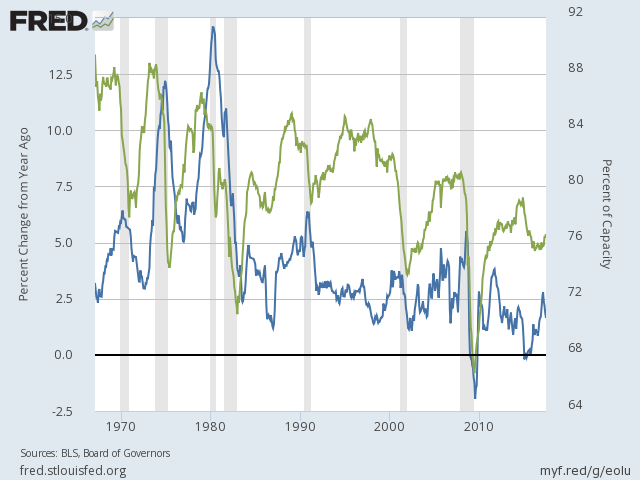

Inflation is currently in the Goldilocks zone, right around 2%, with wage increases also around that level. One indicator we track that tends to warn of increasing inflation is capacity utilization, which measures the proportion of potential economic output that is actually realized, or slack in the economy. You can see from the chart below that inflation (blue line, left axis) doesn’t typically start to accelerate until capacity utilization (green line, right axis) crosses over 80. At the current utilization rate, it would be surprising to see inflation accelerate meaningfully.

Of course, there are many other factors at play. For instance, the two high inflationary spikes in the ‘70s (see blue line above) were largely caused by oil supply shocks which sent oil prices through the roof. Interestingly, we’ve had the exact opposite situation over the last few years. Oil supply has grown, which has driven the price of oil down helping to keep inflation low. Given the emergence of the U.S. as a major energy producer, we don’t see this dynamic changing considerably.

It’s for these reasons, among others, we believe inflation won’t accelerate significantly in the near future. As always, we will keep an eye on the situation and make necessary portfolio adjustments should these views change.

If you have any questions, please don’t hesitate to reach out to your advisor.

Statistics are sourced from the St. Louis Federal Reserve.

This information is provided for general purposes and is subject to change without notice. The information does not represent, warrant or imply that services, strategies or methods of analysis offered can or will predict future results, identify market tops or bottoms or insulate investors from losses. The information has been obtained from sources considered to be reliable, but it is not guaranteed. Past performance is not a guarantee of future results.

Securities and advisory services offered through Geneos Wealth Management, Inc. Member FINRA/SIPC. Advisory Services offered through TPG Financial Advisors, LLC, a Registered Investment Advisory Firm.