Listen to John Woolley, Managing Director of Wealth Management and Chief Investment Officer, and Stuart Robertson, Portfolio Manager, discuss what happened with bonds in 2022 and then read their accompanying commentary below.

We can finally turn the page on 2022, which ended up being a challenging year for almost every type of investment. Last year was unique in that it ended up being just the third year since 1950 where stocks and bonds both posted negative returns. The year was especially bad for bonds, down 13%. Since the 1970s, the worst year for bonds, prior to 2022, was in 1994 when bonds were down 3%. For our commentary this quarter we will review what happened to bonds in 2022 and reasons to be optimistic 2023.

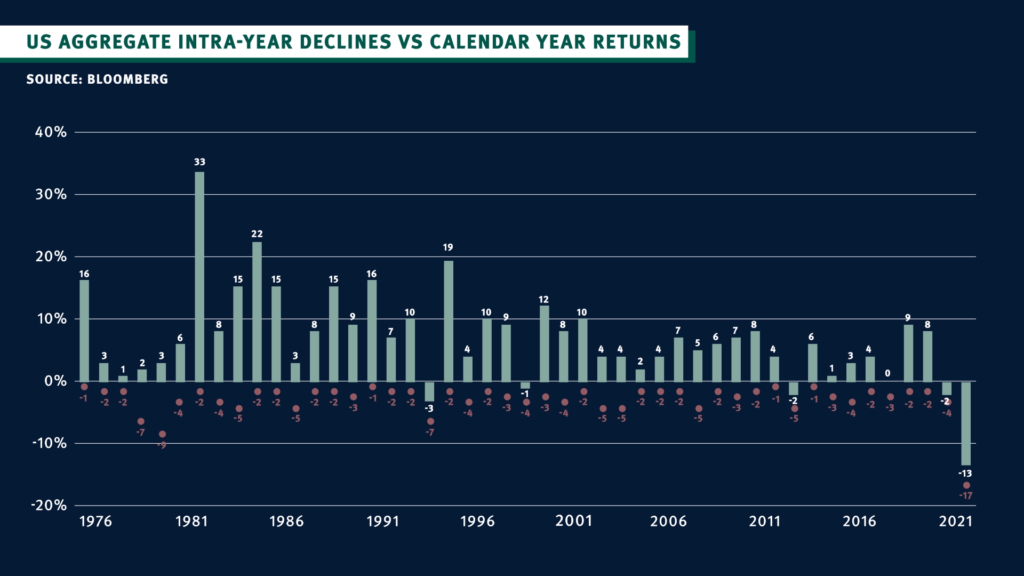

Simply put, we buy bonds in portfolios because they are not stocks. Stocks exhibit superior growth over the long run, but also have higher volatility. Bonds typically are the steadier piece to portfolio composition; they do not have the upside potential of stocks, but they also do not usually have the downside potential, either – all while providing nice cash flow along the way. In 2022, that certainly was not the case with bonds as they were down as much as 17% on an intra-year basis. In prior years, the average intra-year decline was just 3.4% (Fig. 1).

Figure 1. US Aggregate intra-year decline vs. calendar year returns.

So why did bonds perform so poorly in 2022? For that answer, we must look to the Fed and interest rate policy. The return for bonds is dependent on numerous factors, but in 2022, interest rate policy was the catalyst for their poor performance.

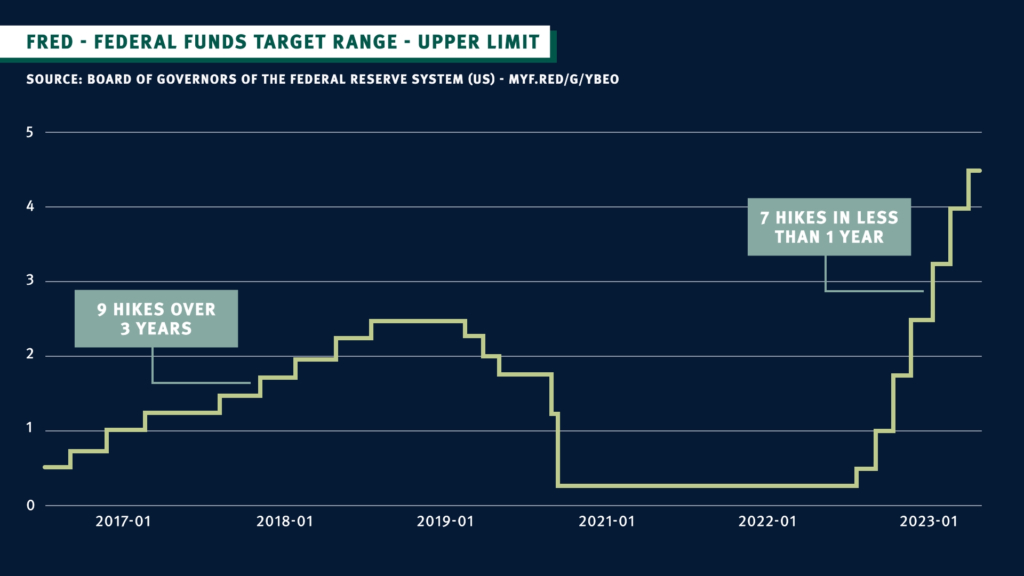

Going into 2022, there was one certainty: interest rates were going to increase. The Fed was crystal-clear from the get-go that their main objective was to cool high inflation. Consequently, 2022 saw the most rapid rise in rates in history. There were seven rate increases in the Fed Funds rate with most of them being 0.75%, leaving the Fed Funds target rate at 4.25–4.50%. However, there is nothing extreme about that level. What was extraordinary was the pace of how it got there (Fig. 2). Compare this rate increase cycle to past cycles that averaged 21 months in duration and had average increases that were typically just 0.25%. In those cases, the average ending point for Fed Fund Target rate was 6.90%.

Figure 2. Fed Funds Target from 2013–2022

In a rising-rate environment, it is advantageous to hold shorter maturity bonds, and this is what we did with our bond portfolios for clients. As bonds mature, we reinvest the proceeds into new bonds reflecting the new, higher yields. While shorter maturity positions can be extremely helpful in a rising-rate environment, they can be a drag on performance when rates fall. Our view is that given the Fed’s aggressive past actions, we are closer to seeing interest rates falling than we are to seeing rates continue to jump up. Considering this, we have begun to slowly adjust bond portfolios to reflect that, increasing the length of our bond maturity dates slightly.

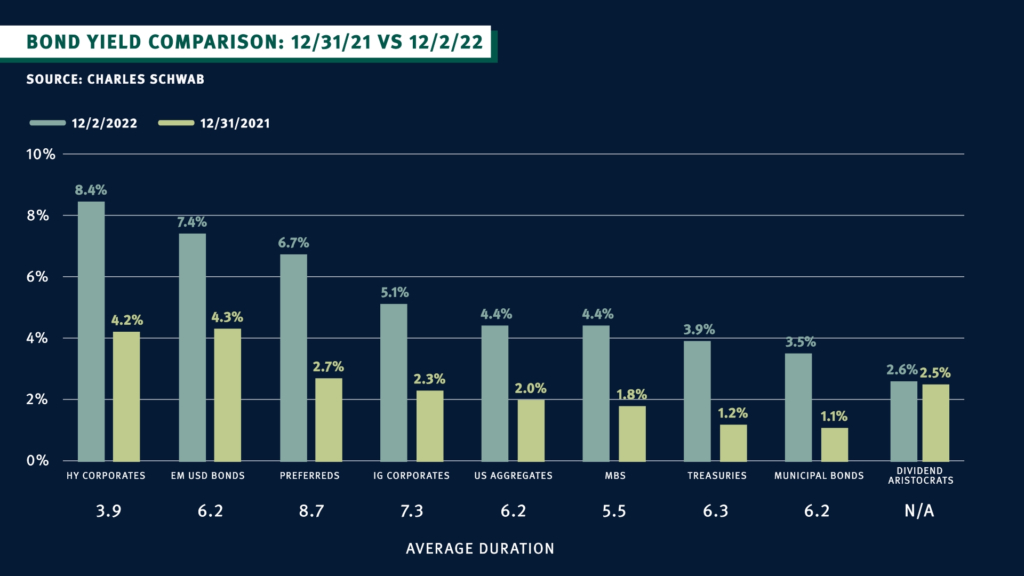

With that in mind, we are optimistic about bonds going into 2023. When bond prices decline, yields (and, thus, cash flows) increase. Given our outlook that the Fed is closer to the top of this rate cycle, we believe most of the pain has been felt in the bond market, leaving attractive yields as we enter the new year. In Figure 3, we see where yields started and where they finished the year for various bond instruments. In most cases, yields doubled during 2022, and even the yield of the bond component of our client portfolios has gone from approximately 2% to 6% as of this writing. The result will be higher cash flows for our clients that we have not seen in many years.

Figure 3. Bond Yield Comparison 12/31/21 vs. 12/2/22

We believe 2022 will be an outlier year for bonds and that they will return to their steadier ways. For the past decade, stocks have experienced above average results in the recent low-yield environment. As a result, stocks did the heavy lifting in most portfolios, providing the bulk of annual returns. We do not expect to return to such a low interest rate environment anytime soon. In this new environment, we think bonds will contribute to overall portfolio returns through their higher cash flows. Time will tell how quickly this happens, and rates can always go up a bit more in the near term, but we think the time has come for bonds to contribute to the cash flows we used to enjoy in years past.

We appreciate the trust and confidence you place in us and do reach out with questions at any time. As always, we love hearing from you!

Stuart Robertson and the TPG Investment Committee

CONTACT THE WEALTH MANAGEMENT TEAM

"*" indicates required fields