Benjamin Franklin once said, “Nothing is certain except death and taxes.” Today we are going to discuss a combination of those two very certain things – also known as the Estate Tax. The Tax Cuts & Job Act of 2017 (TCJA) effectively doubled estate tax exemption thresholds, and as things stand today, you can currently exclude up to $13.6 million for single filers and $27.2 million for married couples filing joint returns.1 The value of estates above these thresholds are taxed at estate tax rates. Just as personal income tax is a progressive tax, so is the federal estate tax, with the top tier for federal estate tax starting at 40% of assets over a $1 million threshold. Many states also impose their own estate taxes. For example, Oregon exempts the first $1 million of an estate, but taxes thereafter range from 10–16%. Washington exempts a higher amount ($2.2 million) with a higher tax rate of 10–20%. These thresholds apply to both single and married couples.

If current tax law does not change, the TCJA will expire in 2026, reverting to the lower thresholds in place in 2016 of $6.46 million (single) and $12.92 million (married). As you can see, this would have a significant impact on individuals and families who experienced growth in their personal net worth over the last 10 years. While 2026 is still off in the distance, below are a few techniques that can be used to reduce the size of your estate in preparation for potential upcoming changes.

Gifting

The simplest, most straightforward way to lower your taxable estate without engaging with an estate attorney is to gift during your lifetime. Gifts can include property, investments, cash, or anything of monetary value. The downside of choosing this option is lack of control of assets. Once an asset has been gifted, the donor surrenders control.

Individuals can give up to $18,000 per year (married – $36,000) under the annual gift tax exclusion. This gift can be accelerated by giving a lump sum of up to five times the annual gift exclusion amount ($90,000) when applied to a 529 College Savings Plan. A common example of accelerated gifting is a grandparent funding education for a grandchild. For many, gifting is the simplest way to lower their taxable estate.

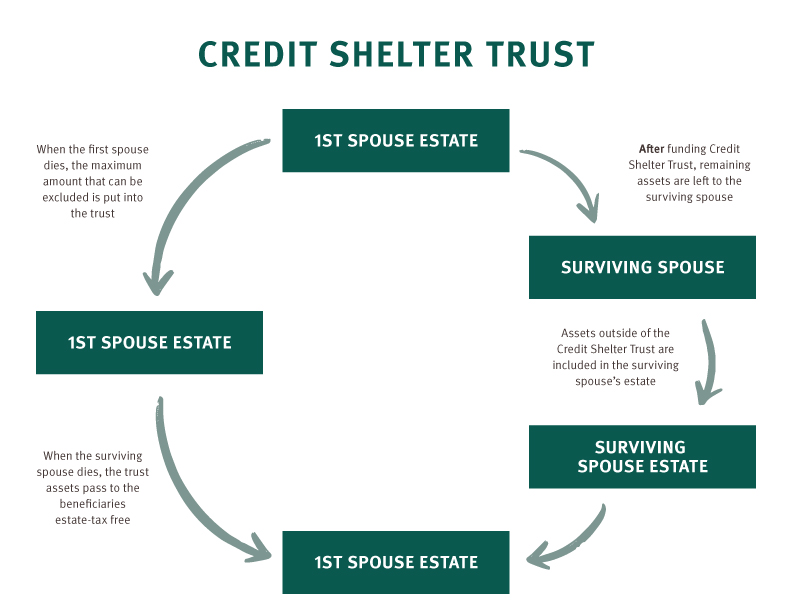

Credit Shelter Trust

A Credit Shelter Trust (CST) is a valuable estate planning tool that can also lower your taxable estate. Different from outright gifting, CSTs allow the donor to maintain more control of their assets. This type of trust can be funded up to the maximum amount excludable under the federal estate tax exemption ($25.84 million).

Let’s take, for example, a couple in Oregon who have a $10 million net worth:

When the first spouse dies, assets designated in the trust document are placed into a Credit Shelter Trust. The surviving spouse doesn’t take control of the assets within the CST; therefore, the designated assets are not included in the surviving spouse’s taxable estate.

In our example, the first spouse can designate, say, $5 million to be placed into the CST upon death. Even if these assets were to grow to $7 million while inside the CST, they would not be taxable, as they are considered outside of the surviving spouse’s taxable estate.

In this case, the full amount within the CST would pass to the beneficiaries tax-free once the second spouse dies. Assets not included in the CST would be subject to Oregon state tax on amounts over the $1 million threshold. If a CST was not used in this example and the TCJA sunsets, the couple’s estate would be valued at $12 million and would be subject to estate tax at both the federal and state level.

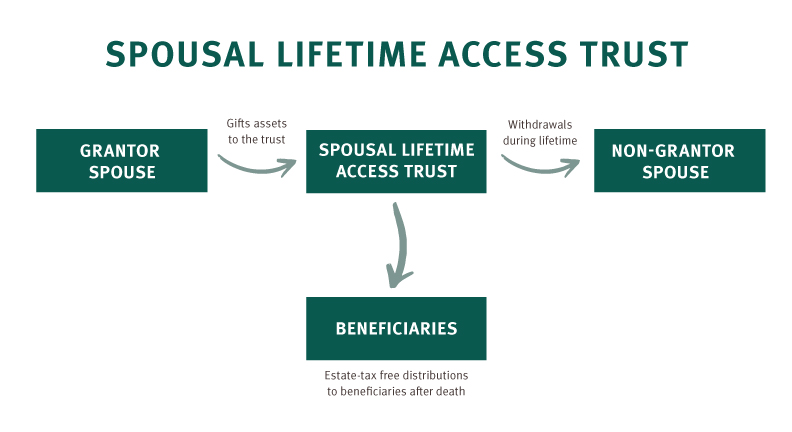

Spousal Lifetime Access Trust

Another alternative to lowering your taxable estate is a Spousal Lifetime Access Trust (SLAT). SLATs are irrevocable trusts where a spouse gifts assets for the benefit of the other spouse. SLATs differ from CSTs as they are funded while both spouses are alive. A unique benefit of the SLAT is that the receiving spouse can access the trust assets while the donor is alive. In certain circumstances, the receiving spouse can receive distributions from either the principal or income generated by the trust.

Let’s look at another example of a couple who live in Washington with a $10 million estate.

One spouse can designate $5 million to be placed in the SLAT. This will immediately lower their taxable estate from $10 million to $5 million.

If these assets were to grow to $7 million inside the SLAT, the growth is not subject to taxation as it is separate from their estate. If the receiving spouse takes $1 million over her lifetime from the SLAT, the remaining $6 million would pass to the designated beneficiaries’ tax free. If these assets were not placed into a SLAT, the Washington estate tax would apply to the entire estate value in excess of the $2.2 million threshold.

We aren’t tax or estate experts and can’t predict the future of the ever-changing tax law, but being prepared for upcoming changes is vital for minimizing your estate tax liability. While each client’s situation is different, these techniques may help prepare you for a possible sunsetting of the TCJA in 2026. We encourage you to consult with your tax and estate professionals to see if these strategies could help you.

If you are interested in how these changes may affect your financial future, please reach out to the Wealth Management team at wealthmanagement@tpgrp.com.

1.IRS.gov