Hear John Woolley, Managing Director of Wealth Management, and Stuart Robertson, Portfolio Manager, discuss the Q3 economy and then read their accompanying commentary below.

At the risk of sounding like a broken record, 2022 has been an extraordinarily tough year for the financial markets. To put this year in context, there has only been one other year in which bonds and stocks were both down to close out a year – 1994, when bonds were down 2.9% and stocks were down 1.5%. Today, markets are pricing in the highest inflation in decades, a rapid increase in interest rates, and a potential recession. With those market dynamics at the forefront of most investors’ minds, we thought it would be helpful to revisit where we stand with regards to inflation, interest rates, and recession odds.

Inflation

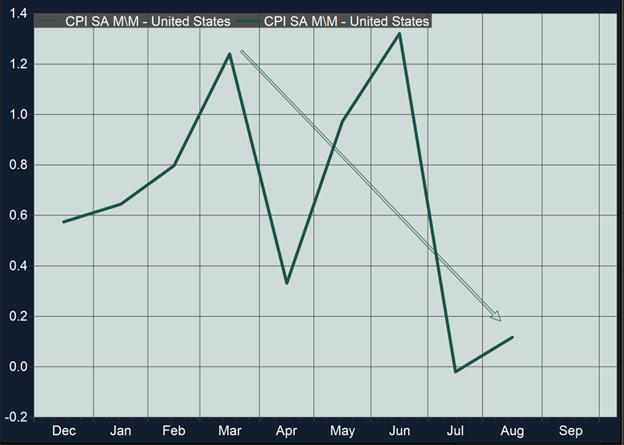

Inflation has run the highest levels we have seen in decades. One can debate the cause (overstimulus, supply-chain disruptions, geopolitical issues) but, simply put, inflation is high and will probably remain so for the near future. However, recent evidence does suggest that inflation may be peaking. The problem, though, is the slide from the peak is proving to be slower than expected. Recent month-on-month data for the Consumer Price Index (CPI) have come in showing more modest increases compared to the earlier months of the year (see Fig. 1). And frustratingly, rarely does inflation fall in as straight a line as we would like. We will still have months that are higher than expectations, and months that are lower than expectations. With inflation being “stickier” than originally expected, the Fed’s reaction has been (and we suspect, will be) for more aggressive rate increases for longer than most had originally anticipated.

Fig. 1 Month-on-Month CPI Data, Dec. 2021–Dec. 2022 (Y-Axis % Change)

Source: FactSet

Fed Policy

As it has been for most of the year, great attention will be focused on the Fed policy in the fourth quarter. The Federal Open Markets Committee (FOMC), the policy-setting committee at the Federal Reserve, will not meet in October, but they will have two meetings left for the year in November and December. We think it likely that they will raise the Fed Funds target rate at both meetings. The magnitude will depend on incoming data during the month of October. If data points to more signs of cooling inflation, it could give the FOMC a window to alter the size of the increases down from 0.75% to 0.50% or even 0.25%. On the contrary, if data shows inflation persistently stubborn, then we expect higher rate hikes on the order of the 0.75% increase we’ve seen the recent past.

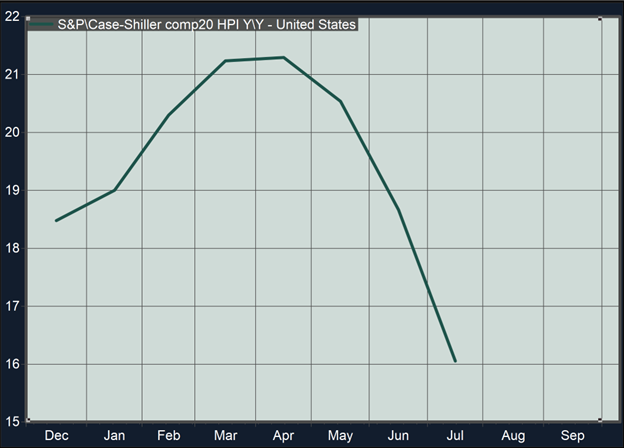

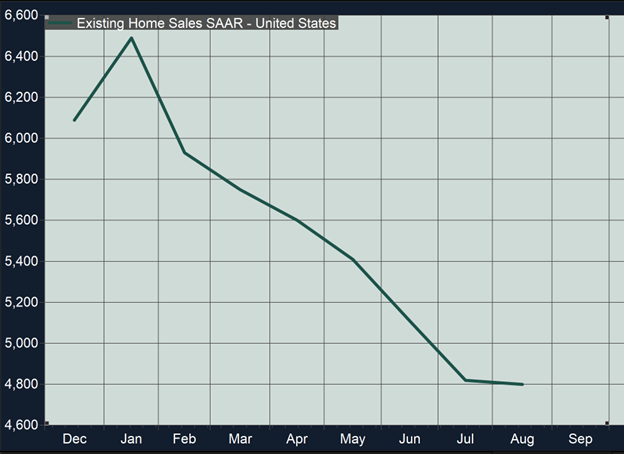

The Fed’s policy is showing signs of working. Consider the real estate market, which had been red hot. Higher housing costs had been putting upward pressure on CPI readings. In recent months, we have seen a substantial drop in both home prices and existing home sales (Figs. 2 and 3). What caused this? Higher mortgage rates. Rates for a 30-year mortgage briefly touched 7% before settling around 6.8% recently, and higher borrowing costs equates to lower demand for houses and, thus, lower prices. With home purchases driving so much consumer spending (think new furniture, painting, yard improvements, tools, etc.), this is the exact outcome the Fed hopes to achieve.

Figure 2. Case-Schiller Y/Y Home Prices (Y-Axis % Change From a Year Ago)

Source: FactSet

Figure 3. US Existing Home Sales, Sept. 2021–Sept. 2022 (Y-Axis Existing Home Units Sold During Month)

Source: FactSet

Recession

Does this mean the economy will experience a recession? A recession is a collection of weaknesses in labor markets, consumer spending, and retail sales – all categories that are still showing strength. It is our view that stock and bond markets have priced in a modest recession. When inflation is this persistent, it is difficult to check inflation without meaningful loss of economic activity that causes a recession. If our economic growth causes an overheating of prices and inflation, it is the Fed’s mandate to step in and pour water on the coals. If the Fed overcorrects to reduce inflation, a recession can certainly be the outcome, but in our view, we are most likely to see only a modest recession.

In Summary

We understand times like these are challenging, but down years in the markets can and do happen. In the history of markets, those who stayed patient were rewarded for their discipline. While we are frustrated by the markets too, we stay focused on the things we can influence: repositioning bonds to generate higher and stronger cash flows because of these higher yields and working to position our equity investments to emphasize those segments that we believe will benefit most when the tide turns.

As always, we value hearing from you most, so please reach out with any concerns, comments, or questions.

CONTACT THE WEALTH MANAGEMENT TEAM

"*" indicates required fields