Portland, Oregon, August 11, 2021 – TRANSITORY. This might as well be the Word of the Year midway through 2021, as inflation accelerates at a pace we have not seen in decades. And if inflation continues at this level, this might even present a risk to the nascent recovery we are starting to see.

In this blog we will examine some of the factors we believe make it transitory, the Fed’s response, and implications for markets.

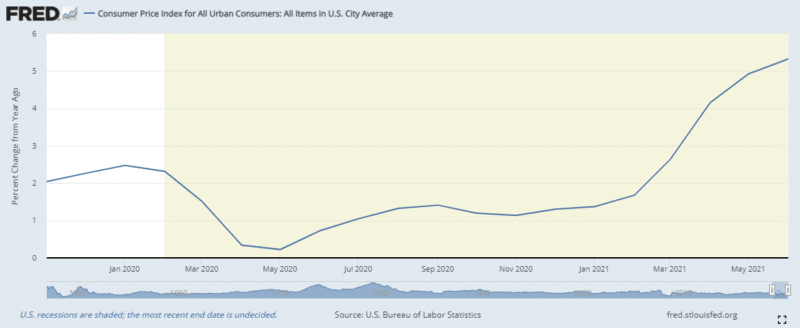

The Consumer Price Index (CPI), a measurement of the change in prices over time using a market basket of consumer goods, accelerated 5.4% on a year-over-year basis during the month of June. This increase was the largest since August 2008. Fed officials have attempted to assuage concerns of investors by describing the surging prices as transitory, or temporary, due to several factors.

Part of the explanation for the surge in prices is skewed by the effects from previous reporting periods. At the onset of the pandemic, prices tumbled, and today’s year-over-year calculation includes those pandemic numbers which had much lower price levels. It might even be more appropriate to describe a good portion of the increase in prices today as reflation (a return to a level) instead of inflation (an increase from a level).

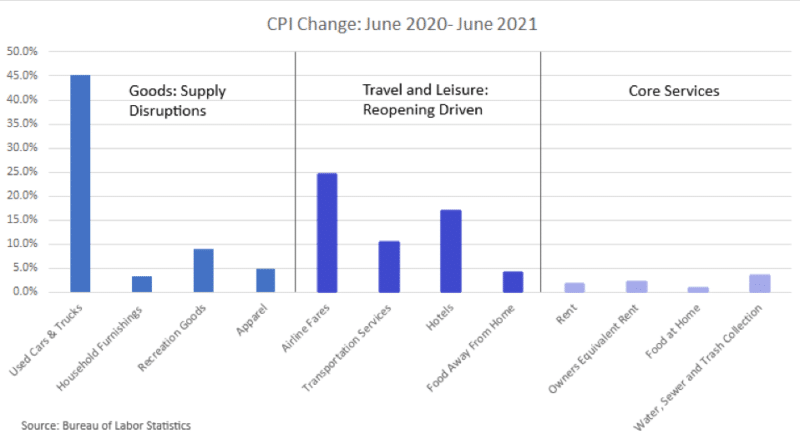

The pandemic also changed spending habits for many individuals. Since there was decreased opportunity spend on services (travel, hotels, etc.), consumer spending shifted towards goods, which caused extra demand for raw materials. This demand strained supply chains around the globe, leading to shortages and price increases. We don’t believe these factors will last forever as economies reopen and consumer spending shifts from goods back to services.

Fed officials, too, seem lockstep in messaging that inflation is transitory. During 2020, in its Statement on Longer-Run Goals and Monetary Strategy, the Fed signaled it will accept periods of higher inflation even though its long run inflation target remains 2%. Economic projections from the Federal Open Market Committee’s June meeting revealed that members’ expectations for inflation had increased, but their projected path of interest rate policy remained little changed, with no hikes to Fed Funds rate expected before 2023. Some economists, though, see a risk that the current Fed might be overlooking the risk of inflation. They fear that in response, rather than gradually adjusting interest rate policy, they would need to sharply act to cool inflation. Capital markets hate surprises, though, and such a swift deviation from current Fed policy could be seen as one. However, considering their comments in minutes released from the June 15-16th meeting, we believe any adjustment to policy outlook is likely to be communicated well in advance.

Financial markets seem to be taking the inflation news in stride, too. Equity markets continued their climb setting all-time highs for major U.S. stock market indices. Typically, equities are a good hedge to modest inflation as they have higher historical returns relative to inflation. Too much inflation, however, can result in higher interest rates, higher input costs, and lower margins: a negative for equities.

Perhaps more notable is the recent decline in bond yields. In recent weeks, the 10-year treasury has dropped to a yield of 1.3%, which seems to communicate the bond market is not worried about inflation. The traditional view is that as inflation rises it erodes the purchasing power of a bond’s cash flows, and investors seek higher-yielding assets pushing bond prices down and yields up. The opposite is occurring now, as a surge in bond buying has pushed yields lower. As it stands, both equity and bond investors appear to agree that inflation is transitory.

Our investment committee is keeping an eye on economic indicators so we can make informed moves to mitigate risk should inflation stick around to be a more permanent guest, but for now we think news headlines will most likely be out of step with the markets. Please reach out with any questions or comments at any time. We appreciate hearing from you.

Stuart Robertson joined The Partners Group in Wealth Management as a Portfolio Manager. Stuart comes to us from Columbia Trust Company where he was an investment portfolio manager for its HNW and institutional clients. While there, he was an instrumental part of the investment committee which was responsible for portfolio strategy and asset allocation. Stuart will sit on the TPG Investment Committee and join us in serving our clients and presenting to prospects.

Advisory services offered through TPG Financial Advisors, LLC, an SEC-Registered Investment Advisor and a wholly owned subsidiary of The Partners Group, LTD.