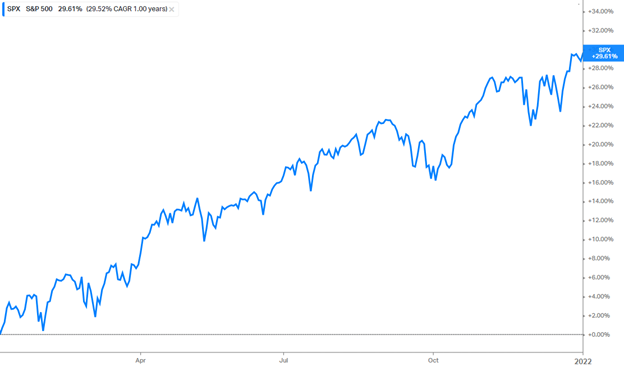

As we write this letter, domestic markets have had a good year and most equity indexes are up double digits. Despite the occasional scary day or two, the year was a relatively calm one (Fig 1). This comes on the heels of a 2020 that saw a 35% decline over just three weeks for the S&P 500 at the start of the COVID-19 pandemic shutdown. Additionally, the fourth quarter of 2021 has been a relatively busy quarter for our trade activity with client portfolios. For each of the last three months our indicators have shifted, requiring the TPG Investment Committee to make appropriate changes to allocations. During these discussions gut feelings and emotions always try to color our thinking, yet discipline wins the day as we remain committed to our process. For this quarter’s letter, we thought it important to share our thoughts on why it’s necessary to check our emotions, ignore gut feelings, and remain committed to the science element of our investment process.

Fig 1. S&P 500 Calendar Year Return through 12.31.2021

Source: Koykin.com

Trusting your gut gets investors into trouble. Consider a quote from legendary investor Benjamin Graham, who said in his landmark book The Intelligent Investor, “The investor’s chief problem – and even his worst enemy – is likely to be himself.” We are our own worst enemy, in part because humans are hard-wired to recognize patterns. As a market increases, the human brain thinks the trend will continue in spite of any contrary evidence. On the flip side, a declining market seems like it will continue to decline. Investing success is keenly dependent on us not allowing emotions to dictate decision making. Left on our own to make decisions, the prevailing tendency is to follow a herd mentality, selling in panic times and chasing performance by buying funds or stocks that are leading the market on the way back up.

Peter Lynch, who served as Chief Investment Officer of Fidelity’s flagship Magellan Fund from 1977 to 1990, returned a staggering 30% on an annual basis during that time. However, a study by Fidelity and the University of Virginia in 1995 found that individuals who invested in the Magellan Fund only achieved a return of 7% based on holding period data. It’s an extreme example, but it illustrates investors’ propensity to buy into funds that are “hot” and avoid those that are down. It’s easy to say the words “buy low and sell high,” but it is much harder to do in practice.

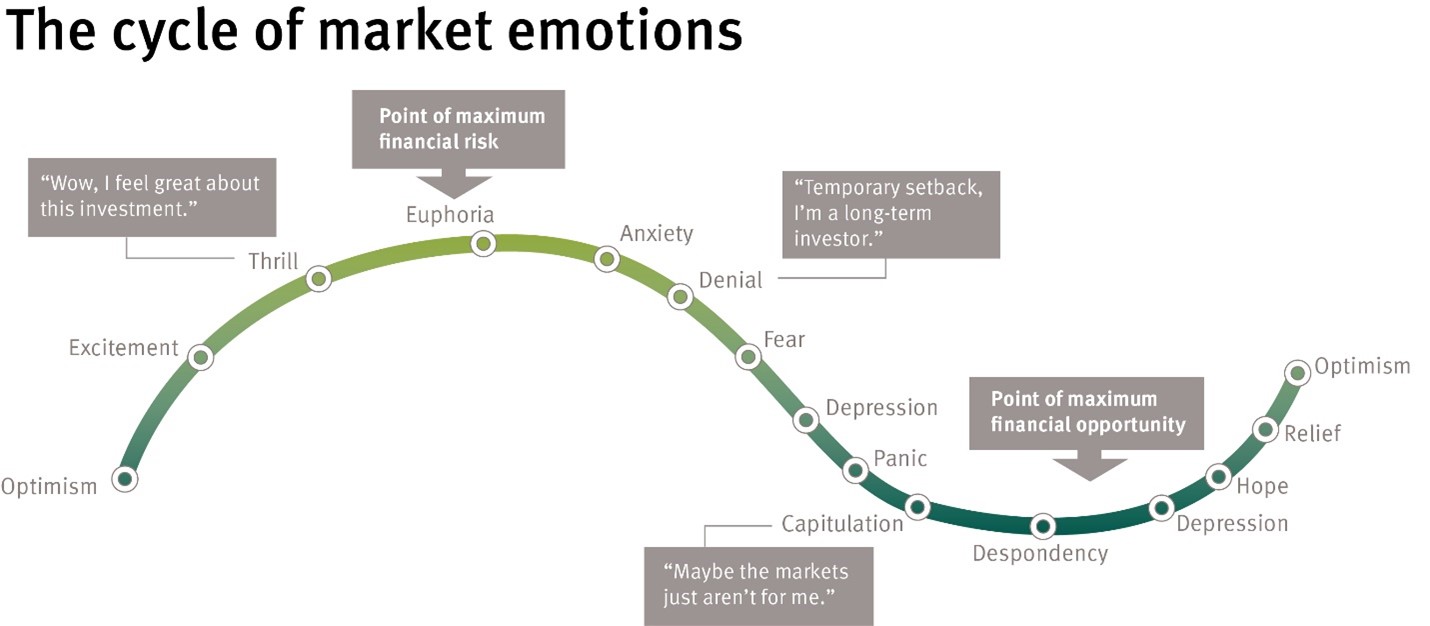

Fig. 2.

Source: CFA Society

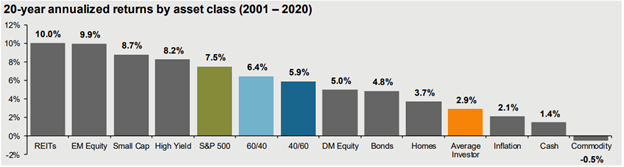

Human emotion towards market risk can be broken down simply: we don’t like losses and will act irrationally to avoid them. Studies have shown that a 10% loss feels equivalent in pain to the joy of a 20% gain.1 Said another way, we feel the pain of losses more than twice as much as we feel the pleasure of gains. This explains why in study after study, the average investor fails to capture market-like results. The DALBAR study below (Fig 3) consistently shows that the gap between what an investment returns and what an actual investor generates is quite significant, often as much as 3–4% annually!

Fig 3.

This is where professional investment management has a unique advantage. Many think the most important value a professional investor brings is security selection or navigating the zigs and zags of the market. And while we do think it’s important to recognize times when it’s appropriate to go on offense and put more to work in equities or play defense and take some risk off the table, we choose to follow our economic indicators to guide that. If we don’t, we risk making emotional decisions. Our client accounts are managed to an investment model that has allocations based on numerous factors, such as a client’s specific goals, objectives, and time horizon, precisely so we will not succumb to our emotions and be tempted to pull completely out of the market in times of panic.

Behavioral finance author Nick Murray is fond of saying an investment management fee is a type of insurance against making a big and costly mistake.2 While no investment manager can insure against losses, putting space between your emotions and your investment decisions can help protect against making a rash decision, like exiting the markets altogether during periods of volatility. That might feel good in the moment but is very damaging to long-term investing success. Breaking bad habits and ignoring your instincts can be difficult. Losses are all but unavoidable when fear takes control, but, through data-driven investment decisions and professional investment advice, those big mistakes can be avoided.

We are humbled by the trust placed with us, and we encourage you to reach out anytime you have questions. Here’s to a great 2022!

***

- “Prospect Theory: An Analysis of Decision Under Risk” by Daniel Khaneman and Amos Tversky, March 1979.

- “Behavioral Investment Counseling” (1st) by Nick Murray, January 2008.