This video segment and article summary includes trends and tips for employers on how to help employees define their retirement plan goals, how to use plan design to help them establish and meet those goals, and financial wellness. Additional related videos include: Attracting and Retaining Quality Employees – Part 1, Recent Trends in Traditional & Non-Traditional Employee Benefits and Benefits Communications Strategies.

As presented by Gary Alton, Managing Partner of the Employee Benefits division at The Partners Group, and Nicole Pond, Managing Consultant and Retirement Plans Partner at The Partners Group.

Top trends in employee retirement plans

Defining plan goals:

The key with helping employees is to talk with them and address these questions “How do you want this retirement benefit to work for you? Where are you at today? Where do you want to be and how do we get you there?”

Plan design:

We’ve learned from a retirement readiness and financial wellness perspective that we need to do more than talk about fees, funds and fiduciary obligations to get people to retirement. It’s really about how do we put those plans in place by talking with our clients on what those goals are and how we use plan design to get there.

Automatically enroll all employees, not just new hires

Some key trends of retirement plan design are automatic enrollment and automatic escalation. This addresses how we get people to save earlier. The key contributor to people having a successful retirement is starting to save at an earlier age and starting to save at an appropriate level. Automatic provisions are starting to get us to that point which is why we’re starting to see many clients adopting it.

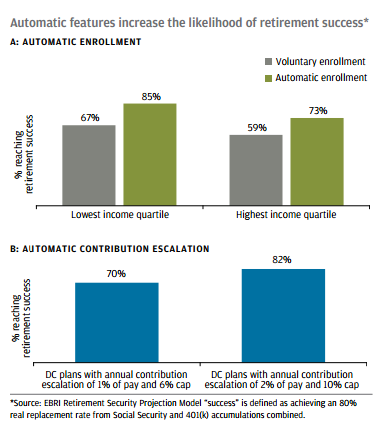

In this study by EBRI, we can see voluntary enrollment versus automatic enrollment for lowest income quartile employees. If they’re left to their own accord to enroll, we see a 67% success rate of reaching retirement versus an 85% success rate with automatic enrollment. Retirement is defined by EBRI for those that are achieving an 80% real replacement rate return, also including social security. Additionally, there is a 59% success rate with voluntary enrollment compared to a 73% success rate with automatic enrollment for those in the highest income quartile.

According to EBRI, 70% will reach retirement success if they are automatically increasing contributions at 1% a year, versus 82% if they are increasing contributions at 2% a year to that cap of 10%. So instead of escalating at 1% to a cap of 6%, we can escalate employees at 2% a year to a cap of 10%, helping them achieve their goals. It’s really just looking at the plan differently. We hear a lot from clients who are concerned that it feels too paternalistic. However, the reality is when you look at your new employee base and go back to some of the previous data we looked at in part 1, we’re seeing employees and especially Millennials want that guidance and coaching. They’re actually thanking employers for helping them start sooner because they feel overwhelmed by the process.

Financial wellness:

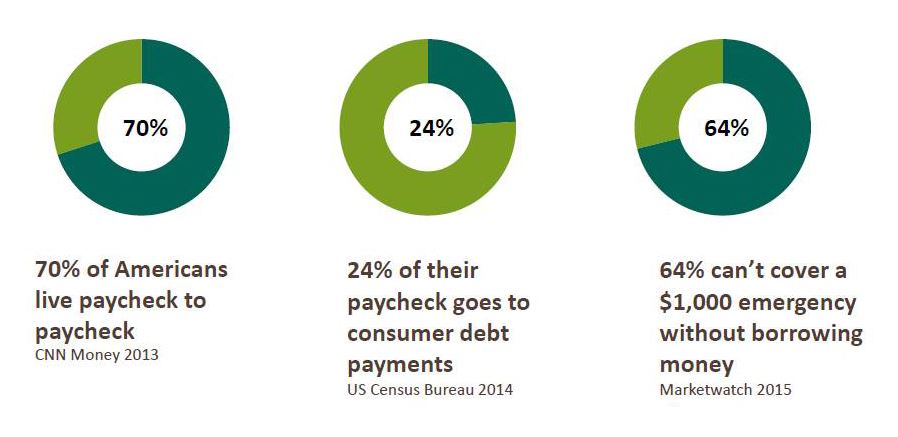

70% of Americans are living paycheck to paycheck. In 2014 24% of employees’ paychecks was going to consumer debt such as payday loans, credit cards, etc. 64% couldn’t even cover a $1,000 emergency. These are key critical issues that are impacting the workforce, which also impacts productivity.

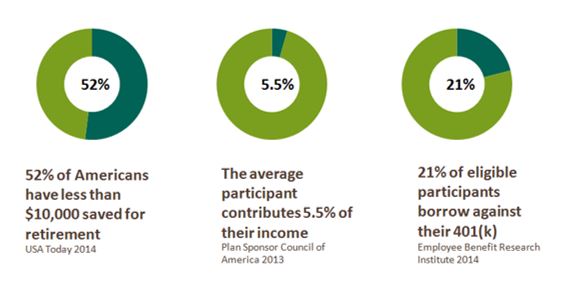

52% of Americans have less than $10,000 saved for retirement. Then when we think about the average contribution rate from an employee into a plan, it’s only 5.5% of their income. We know that to get to retirement, 5.5% of our income isn’t going to be enough to get us there. Also a hot topic with a lot of our clients is whether or not to allow retirement plan loans. This data tells us 21% of eligible employees borrow against their 401(k). Instead of using the 401(k) plan as the vehicle to save for retirement, they’re looking at it as more of a short term concept which devalues their account as they get closer to retirement.

Wrap-up

Here are a couple things to consider:

- Number one, the cost to replace a quality employee can be 20% or more of their annual salary. Depending on your turnover and your workforce, this can be a huge hidden cost that a lot of employers aren’t even tracking. When you think about the cost to find a new employee, to train them, the time it takes to get them up to speed in the job, and to build that institutional knowledge, it could take years in some cases, and retention is critical.

- Benefits are clearly re emerging as a competitive advantage in the marketplace. In the Pacific Northwest, we have unemployment less than 5%, and that is heating up the competition in the job marketplace. Benefits are critical to attracting and retaining quality employees.

- More complex/easier to administer: As things get more complex, as employers offer more benefits, it is important to make it easy to administer. With communication, enrollment, tracking adds and deletes, it’s going to be critical to simplify the overall enrollment process. That is where we see those online enrollment platforms becoming more and more critical every day, even down to smaller employers under a hundred lives.

Links to continued segments of this article and videos: Attracting and Retaining Quality Employees – Part 1, How to Effectively Communicate Your Benefits Package to Diverse Employee Demographics and Recent Trends in Traditional & Non-Traditional Employee Benefits.

The Employee Benefits Division of The Partners Group serves the employee benefit needs of over 500 West Coast employers, with offices in Portland, Lake Oswego, and Bend, OR; Bellevue, WA; and Bozeman MT. Our benefits consulting team specializes in providing a highly-consultative approach coupled with problem-solving wellness analytics, to help employers reduce healthcare costs, improve employee health, and create long-term health plan stability.

We focused on employee benefits in this article, however The Partners Group works through four different divisions all coordinated together, with services also including wealth management, investment planning for individuals, commercial and individual insurance, and we have business consulting which is more for project based work.

Securities and advisory services offered through Geneos Wealth Management, Inc. Member FINRA/SIPC. Advisory services offered through TPG Financial Advisors, LLC. a Registered Investment Advisory firm.

Presented By:

Gary Alton – Managing Partner, Employee Benefits, The Partners Group

Nicole Pond – CBFA, Managing Consultant, Retirement Plans, The Partners Group