From time to time the Department of Labor, the Internal Revenue Service and/or the Pension Benefit Guaranty Corporation make revisions to Form 5500.

From time to time the Department of Labor, the Internal Revenue Service and/or the Pension Benefit Guaranty Corporation make revisions to Form 5500.- Revisions made to the 2023 Form 5500 relate to SECURE Act amendments made to ERISA. The changes are intended to improve reporting of financial information and plan expenses. There are new compliance questions concerning safe harbor status and how a plan satisfied certain discrimination and coverage tests.

- A significant change affects the methodology for determining if a plan has less than 100 participants and is, therefore, treated as a small plan exempt from the annual requirement to retain an independent auditor. Under the current rule, all eligible individuals must be counted, even those who elect not to participate. Going forward only participants and beneficiaries with account balances on the first day of the plan year must be counted.

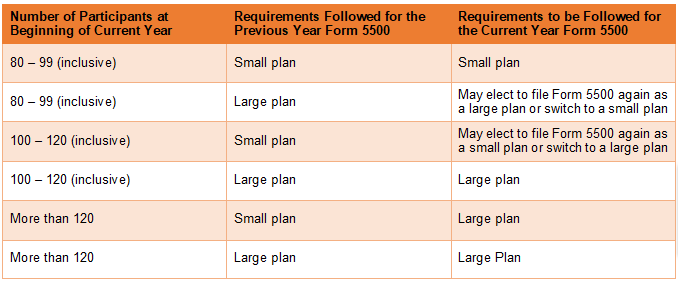

- There is a rule known as the 80/120 rule intended to prevent plans with close to 100 participants from regularly falling within and without the scope of a required audit. Under this rule, a plan treated as a small plan in the previous year will continue to be exempt from the audit requirement if has less than 120 participants. This rule works as follows:

Source: RPAG Fiduciary Hot Topics Q3 2023